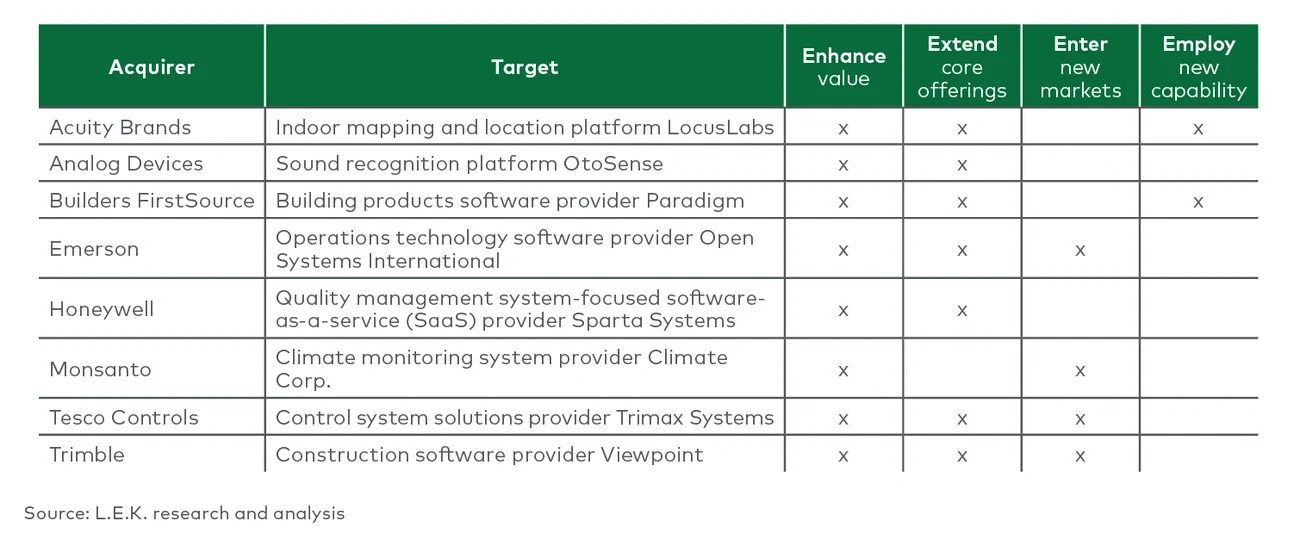

When Emerson Electric and AspenTech announced their $11 billion merger in October 2021, it marked the latest turn in a series of megadeals for industrials software. Just a few months earlier, Rockwell Automation spent $2.2 billion to acquire Plex Systems. And in December 2020, Honeywell International acquired Sparta Systems for $1.3 billion.

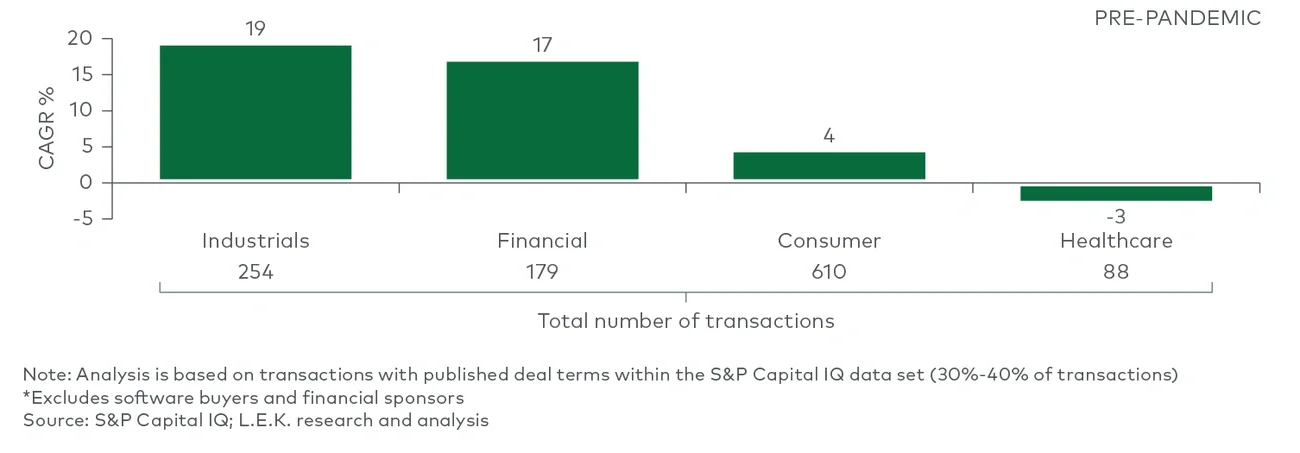

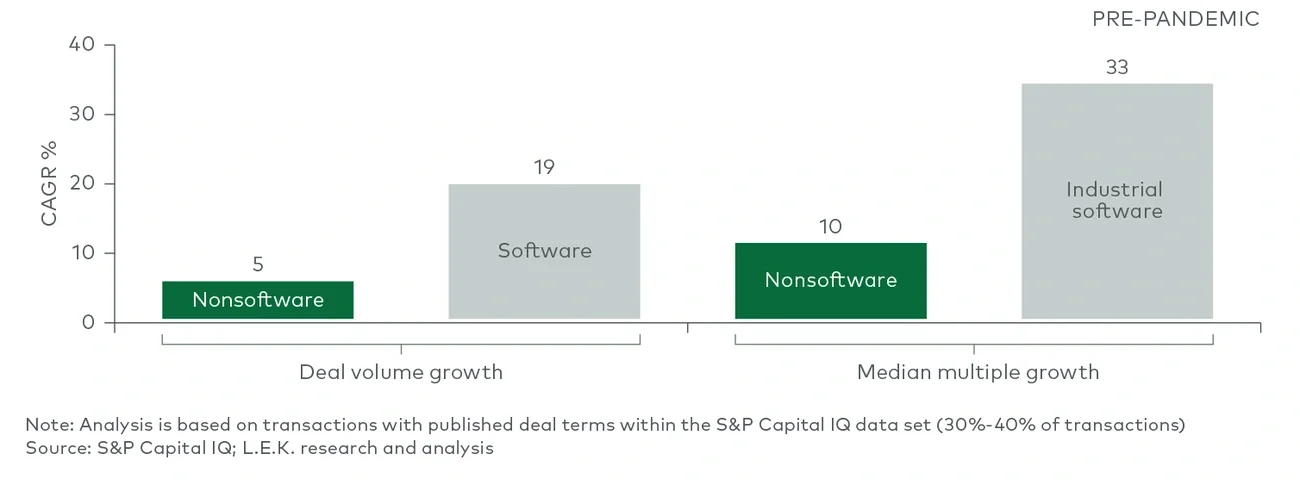

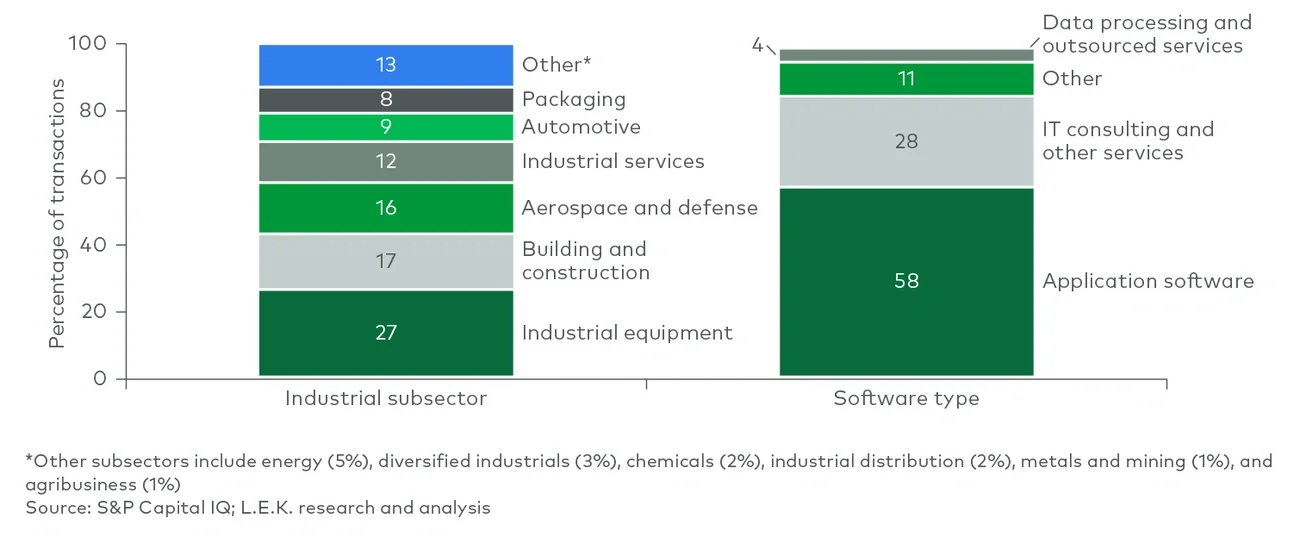

All told, 11 deals each exceeding a billion dollars took place over the three years culminating in Emerson’s announcement. That compares with just two such transactions between 2010 and 2017. Although industrials companies still spend more on equipment makers in aggregate, software accounts for a growing percentage of industrials M&A in the U.S., with growth in software deals outpacing nonsoftware transactions by nearly a 4-to-1 margin.

Accelerating digital adoption

What’s behind this software shopping spree? Industrials companies are diversifying their portfolios in response to a shift toward digital enablement and resulting new profit pools. For example, many companies are looking for solutions that add value to legacy products — think artificial intelligence (AI) for predictive maintenance — or for digital tools that enhance the customer experience. There’s also the opportunity to add software-based services that boost customer loyalty and create stable, recurring revenue streams.

Together, these and other investment scenarios break down along what we call the four E’s:

- Enhance the value of current offerings (e.g., AI for predictive maintenance)

- Extend the portfolio of offerings to include software and promote cross-selling (e.g., automation equipment player acquiring plant operations software)

- Enter new digital markets or business models (e.g., data platform monetization)

- Employ a new digital capability (e.g., tech-enabled service or digital marketplace)

Often a single acquisition can serve more than one objective (see Table 1).