Australia’s economic conditions in 2024 presented significant challenges, impacting the M&A environment. Sector-specific dynamics and strategic investments shaped the landscape. We have made three key observations:

Observation 1

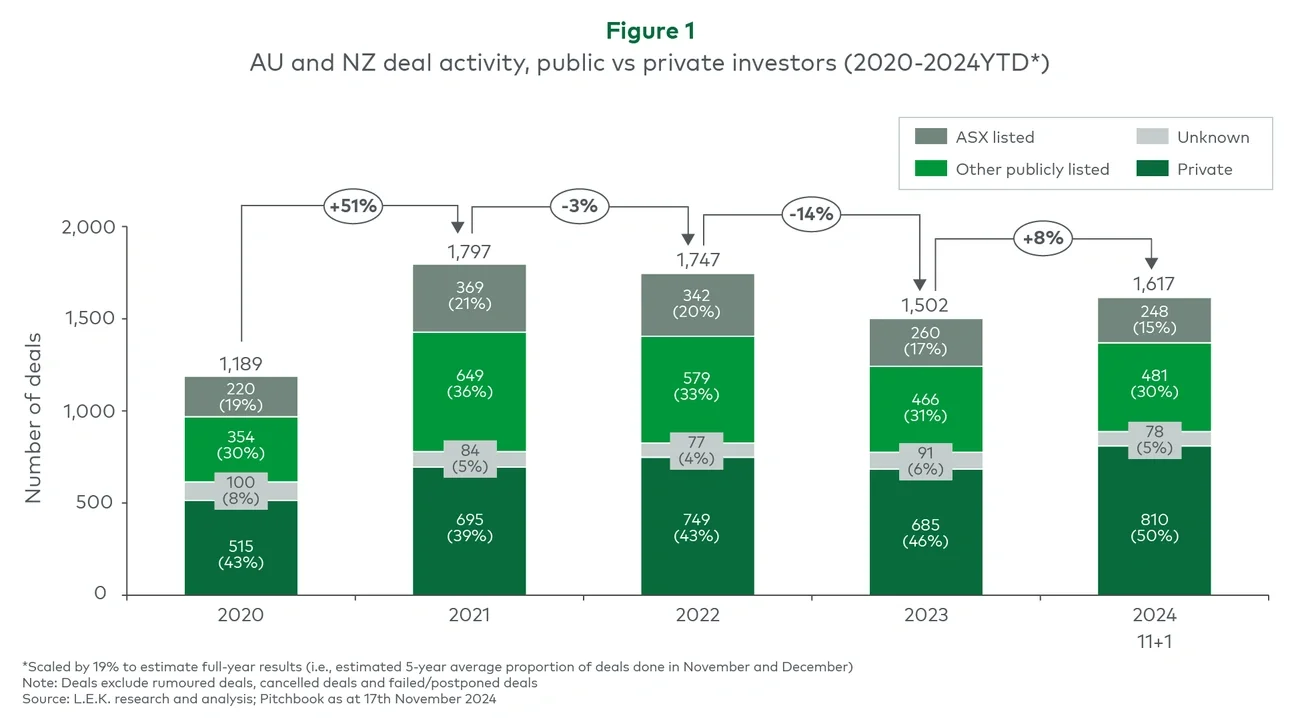

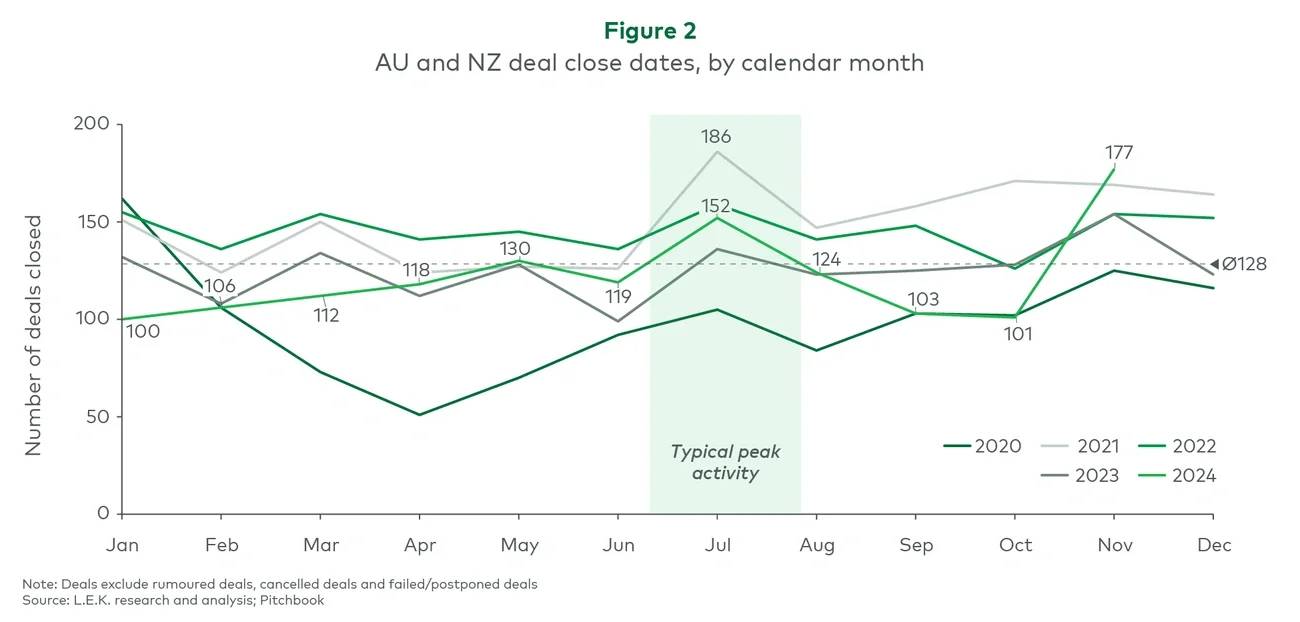

The volume of M&A deal activity in 2024 is likely to be approximately 5-10% higher than in 2023: ANZ deal activity for 2024 remained suppressed after the post-COVID-19 boom years of 2021 and 2022, but it is expected to land slightly above 2023 levels (see Figure 1). There are promising signs of a rebound, as evidenced by the jump in deal activity in Q3-Q4 (see Figure 2):

- In 2024, persistently high interest rates continued to impact financing costs for leveraged buyouts and suppressed appetites for large acquisitions.

- A valuation gap between buyers and sellers persisted, scuppering several marquee transactions in 2024. However, this did not impact all sectors equally. There are signs that this gap is beginning to close and is arguably narrower than that in 2023.

- The increase in activity and rebound during the second half of 2024 can be attributed to easing inflation (e.g., Australian CPI was 2.1% in September compared to 3.8% in June) and a softening labour market, which encouraged consolidation as companies sought to manage costs and remain competitive. November was one of the strongest months since 2021.

- Private capital investors have consistently contributed to a significant volume of deals each year since 2021. In 2023 and 2024, they drove approximately 50% of all transactions, indicating the reliability and resilience of the private capital market in ANZ.

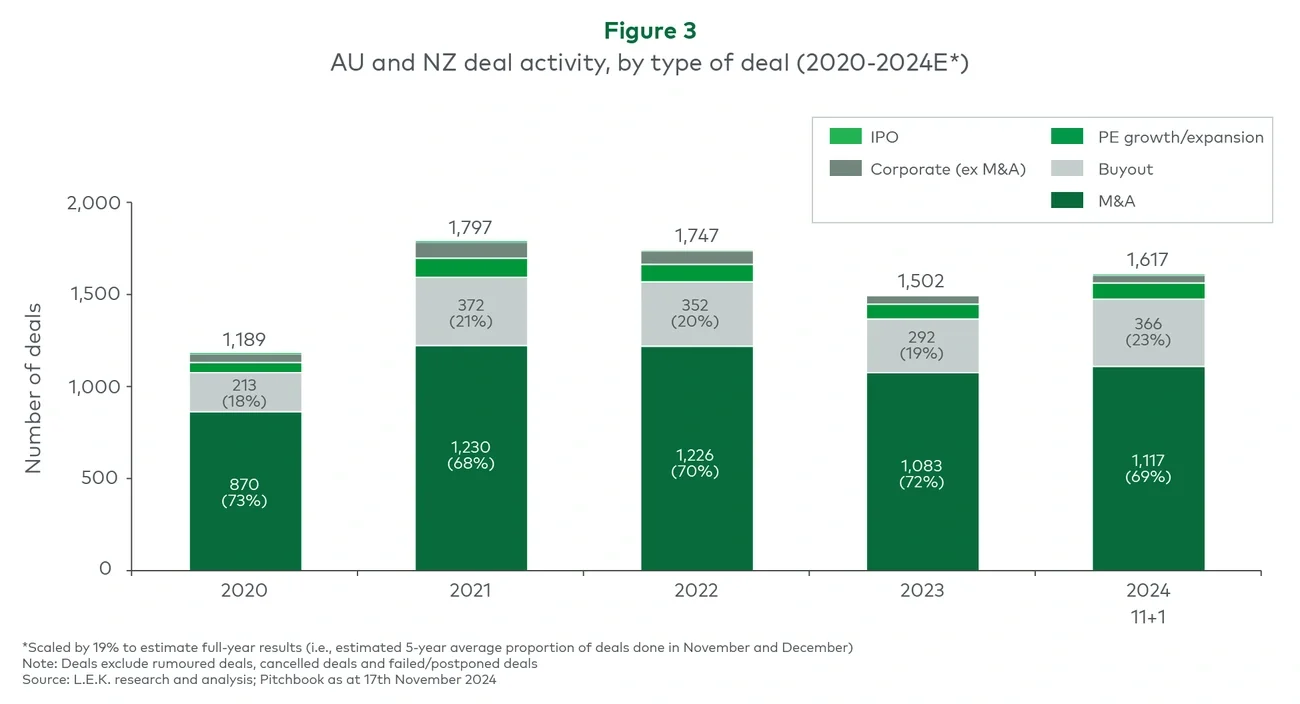

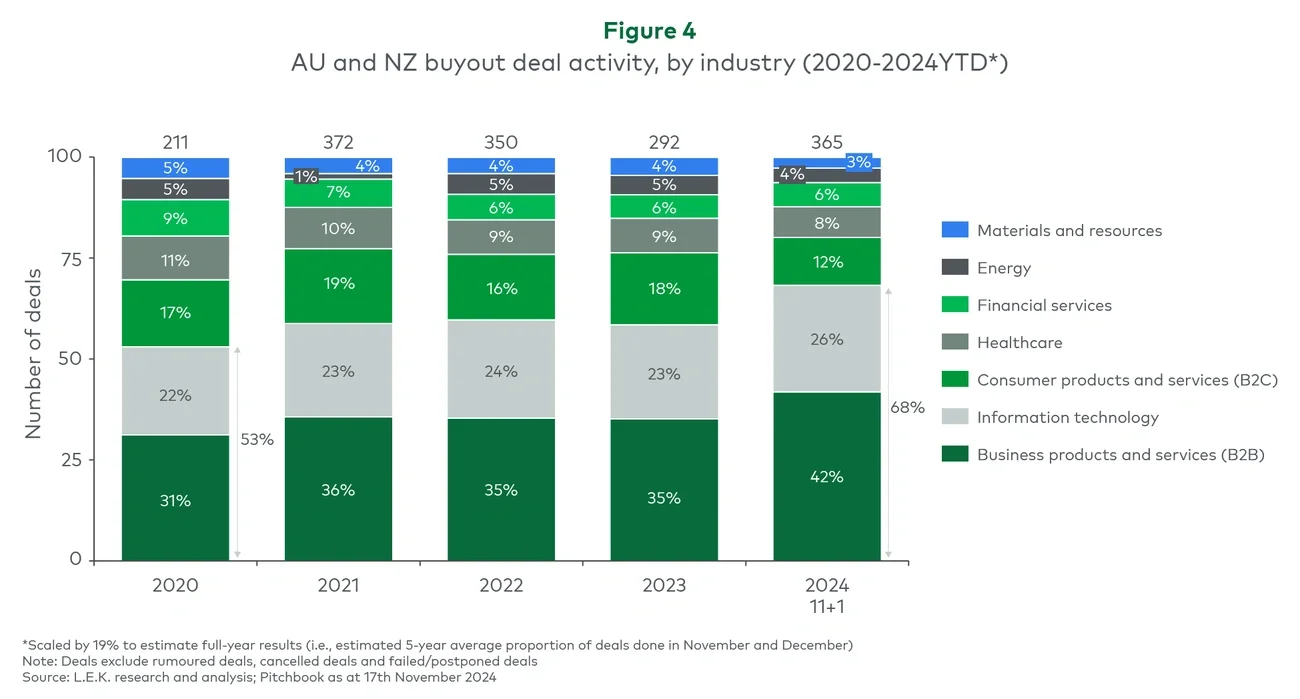

- Could this be a “new normal”? We don’t believe so, as changes in the mix of deal types, industry sectors, and types of investors indicate different expectations and levels of confidence for 2025.